Personalisation

Boostr personalisation adjusts the checkout experience based on who the customer is and what they are buying. Instead of showing every payment option to every customer, Boostr validates eligibility in real time and surfaces only the options a customer can actually complete. The result is a faster, more relevant checkout that reduces failed attempts and increases conversion.

Personalisation also reduces repeat effort for returning customers. Saved cards, preferred UPI apps, and stored addresses carry over across sessions so returning customers can pay in fewer steps than their first visit.

When a customer reaches checkout, Boostr collects context about the customer and the current order. It then runs real-time eligibility checks across payment modes, validates saved instruments, and determines which options to surface. The checkout UI (powered by Sonic) presents only the eligible, validated options so customers never see a payment mode they cannot use.

This eligibility-first approach means fewer payment failures, less customer confusion, and higher completion rates. Personalisation runs automatically when enabled and does not require the customer to take any extra steps.

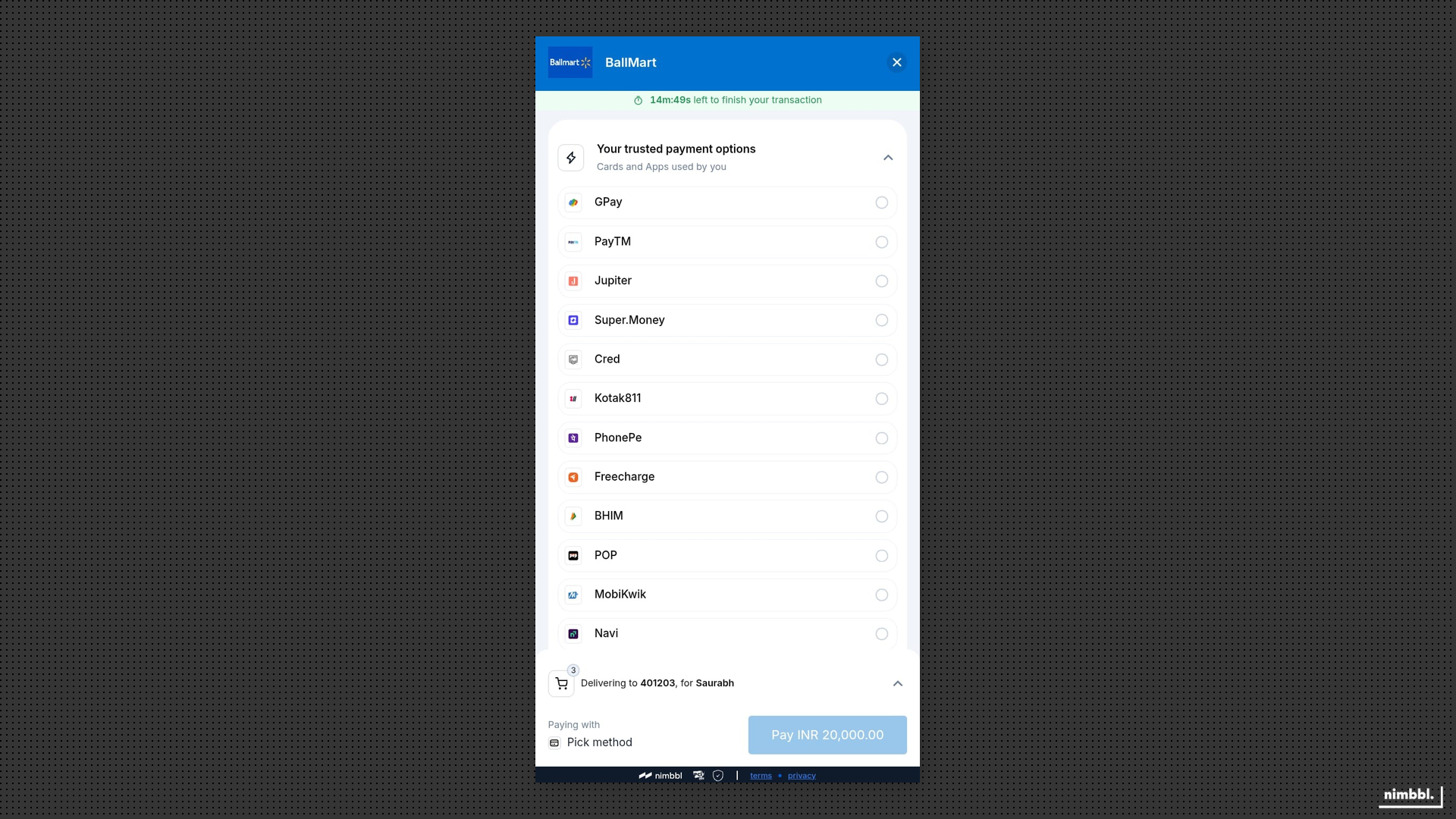

Magik UPI

Magik UPI detects the customer's preferred UPI app and surfaces it as the primary payment path at checkout. The customer sees their UPI app ready to go and can initiate payment with a single tap instead of scrolling through a list of UPI options or manually entering a VPA.

Magik UPI works for any customer, whether they are returning or visiting for the first time. The detection runs automatically and does not require a prior Nimbbl transaction. When the customer's UPI app is identified, it appears prominently in the fast payment tray. If detection is unavailable, Sonic falls back to the standard UPI option list so the payment flow is never blocked.

Magik UPI detects the customer's UPI app and surfaces it first. If detection is unavailable, a fallback list of UPI options is shown so the customer can still complete payment.

For merchants, Magik UPI means higher UPI conversion rates and fewer drop-offs. Customers reach the payment confirmation screen faster, which reduces the window for abandonment. Magik UPI supports major UPI apps and can be enabled or disabled based on your needs.

Magik UPI surfaces the customer's preferred UPI app for faster payment initiation.

Magik UPI surfaces the customer's preferred UPI app for faster payment initiation.

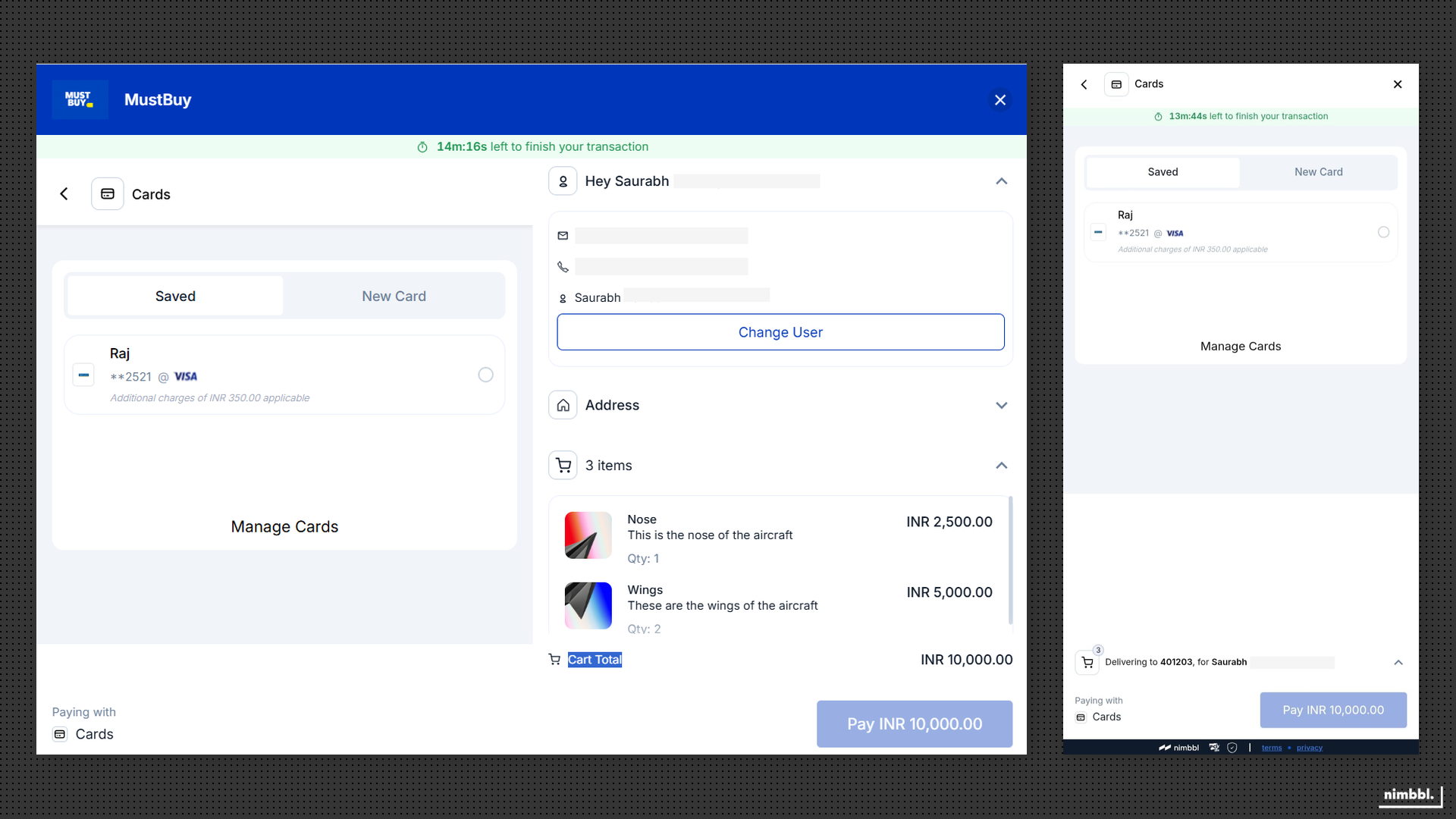

Intelligent Saved Cards Suite

The saved cards suite gives returning customers a faster checkout path by displaying their tokenized card instruments with relevant options. When a customer has previously saved a card, Sonic shows it at checkout along with per-card details such as EMI eligibility and currency conversion options where available. Customers select a saved card and complete payment with minimal input.

Behind the scenes, Boostr manages the full token lifecycle: saving cards securely, validating tokens, and removing cards when the customer requests it. The saved card experience adapts to each instrument, showing only options that apply to that specific card. For example, if a saved card is eligible for EMI on the current order amount, the EMI option appears alongside the card. If it is not eligible, the option is not shown.

For merchants, saved cards drive more repeat purchases and reduce checkout abandonment. Customers who see their card ready to use are far more likely to complete payment than those who need to re-enter card details.

Saved cards appear at checkout with EMI and currency options where applicable.

Saved cards appear at checkout with EMI and currency options where applicable.

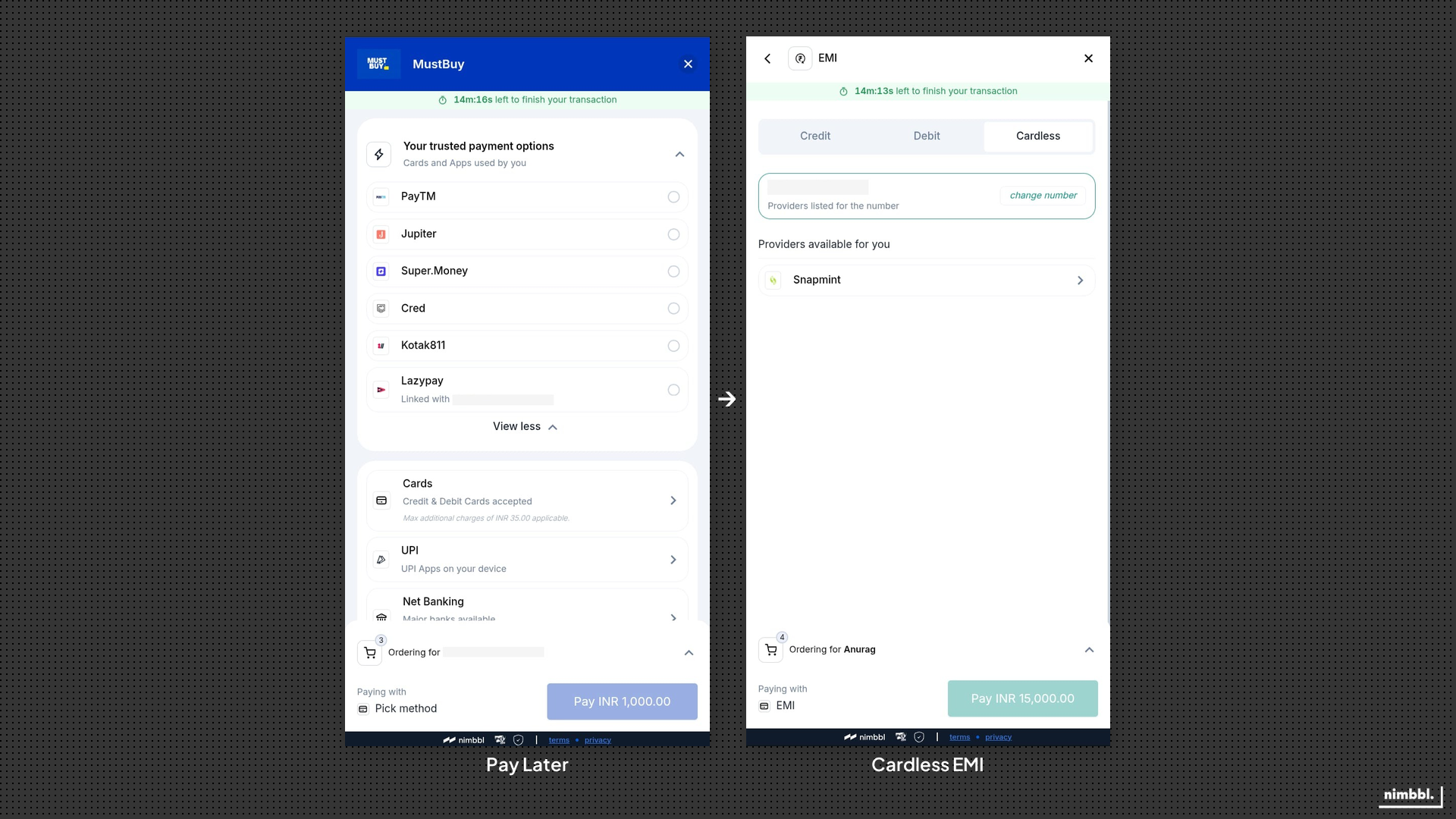

Pay Later and Cardless EMI Eligibility

Boostr validates Pay Later and cardless EMI eligibility in real time so these options appear only when the customer qualifies.

For Pay Later, Boostr checks eligibility with each configured provider (Lazypay, Mobikwik Zip, Ola Postpaid, and Simpl) and filters out any option the customer cannot complete. This prevents the frustration of selecting a Pay Later option only to be rejected during the payment flow.

For cardless EMI, Boostr checks eligibility with configured issuers and schemes based on the customer's identity signals and the current order context. Only eligible issuers and tenures are displayed.

Eligibility is checked in real time for both Pay Later and cardless EMI. If a provider or issuer returns ineligible for the customer or order, that option is not shown. Availability depends on both customer eligibility and order constraints set by the provider.

For merchants, real-time eligibility means fewer failed payment attempts and clearer conversion data. You see actual completion rates rather than attempt rates inflated by ineligible selections.

Only eligible Pay Later and cardless EMI options are shown based on real-time eligibility checks.

Only eligible Pay Later and cardless EMI options are shown based on real-time eligibility checks.

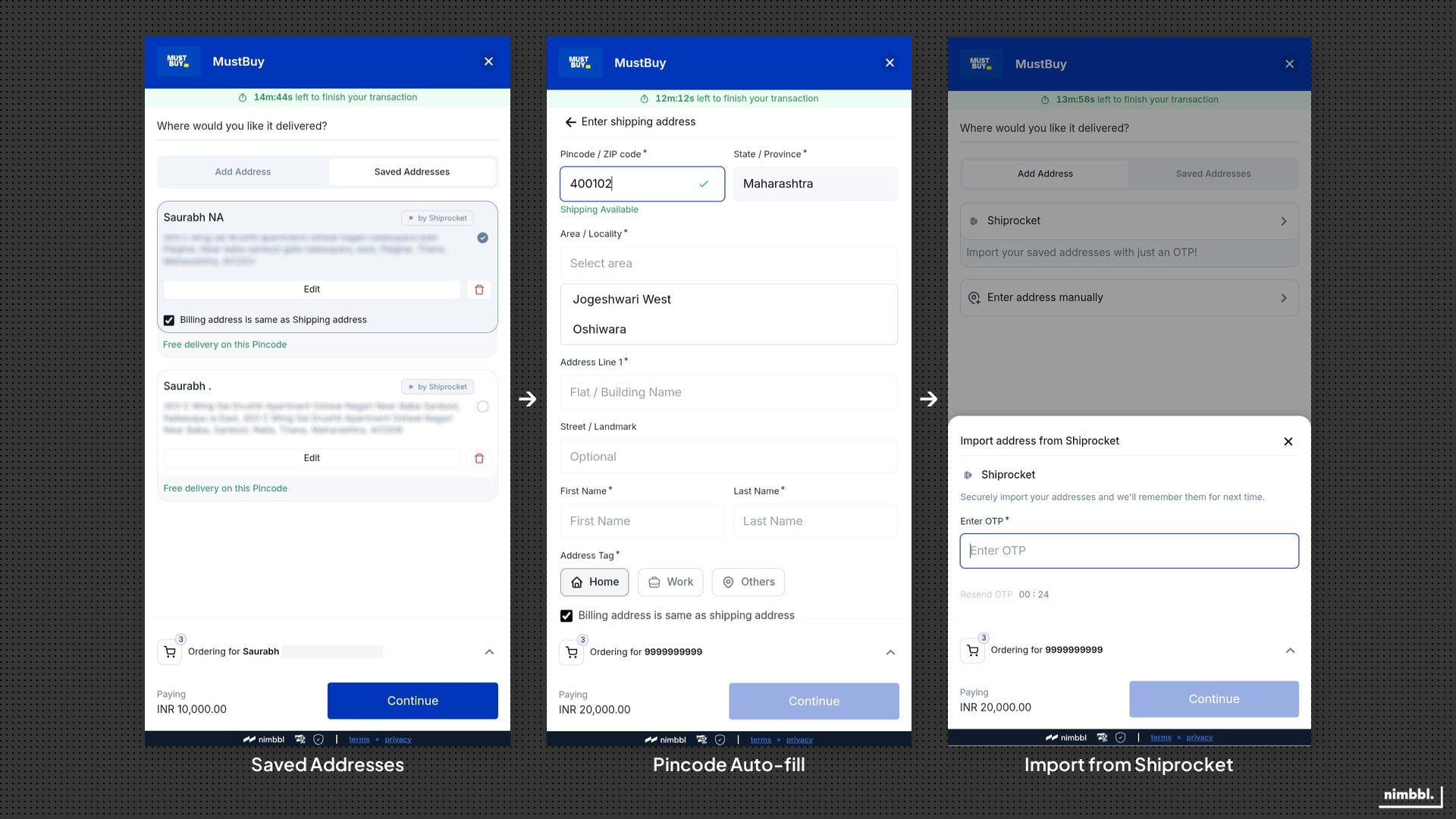

Smart Address Management

Smart address management reduces manual address entry and improves delivery success. When a customer starts the address step, Boostr can auto-fill address fields from connected providers, verify the address through OTP-based validation where required, and check delivery eligibility including COD availability for the entered location.

The customer experience is straightforward: less typing, faster completion, and upfront visibility into whether their preferred delivery option is available at their address. For merchants, better address quality translates to fewer failed deliveries, lower return-to-origin rates, and fewer abandoned carts at the shipping step.

Three address scenarios: saved addresses from prior orders, pincode-based auto-fill, and one-tap import from Shiprocket.

Three address scenarios: saved addresses from prior orders, pincode-based auto-fill, and one-tap import from Shiprocket.

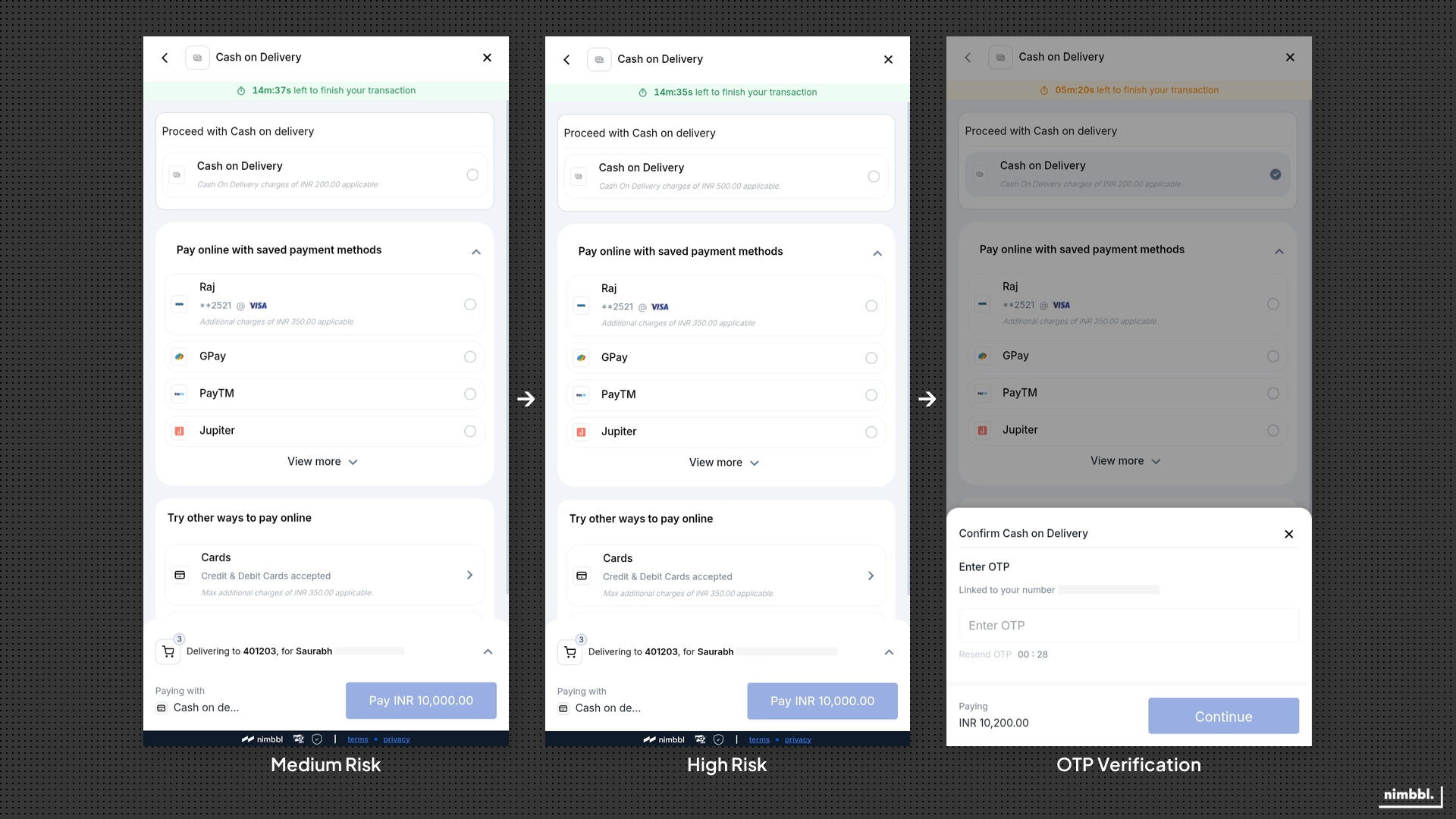

Risk-Based COD Management

Boostr includes risk-based Cash on Delivery (COD) management that adapts COD availability and pricing to each order's risk profile. When a customer selects COD as their payment mode, Boostr evaluates the order and customer context in real time to determine whether COD should be allowed.

Based on risk signals such as customer purchase history, order value, delivery address, and previous COD behavior, Boostr can allow COD at standard terms, block COD entirely, or require a partial prepayment before the order is confirmed. These decisions are made at checkout so the customer sees their COD eligibility and any applicable charges upfront.

For merchants, risk-based COD management reduces COD-related fraud, lowers return-to-origin (RTO) rates, and cuts operational costs associated with failed deliveries. Merchants configure risk thresholds and COD rules based on their business needs, balancing COD availability for trustworthy customers with protection against high-risk orders.

COD visibility and pricing adapt to risk. Merchants can offer COD to more customers while limiting exposure where risk is higher.

COD availability and pricing adapt to the order's risk profile.

COD availability and pricing adapt to the order's risk profile.